In my view, Big Tech Crypto wallets will likely render private fintech blockchains obsolete.#BigTech #CryptoWallet

Quick Video Breakdown: This Blog Article

This video clearly explains this blog article.

Even if you don’t have time to read the text, you can quickly grasp the key points through this video. Please check it out!

If you find this video helpful, please follow the YouTube channel “BlockChainBulletin,” which delivers daily Crypto news.

https://www.youtube.com/@BlockChainBulletins

Read this article in your native language (10+ supported) 👉

[Read in your language]

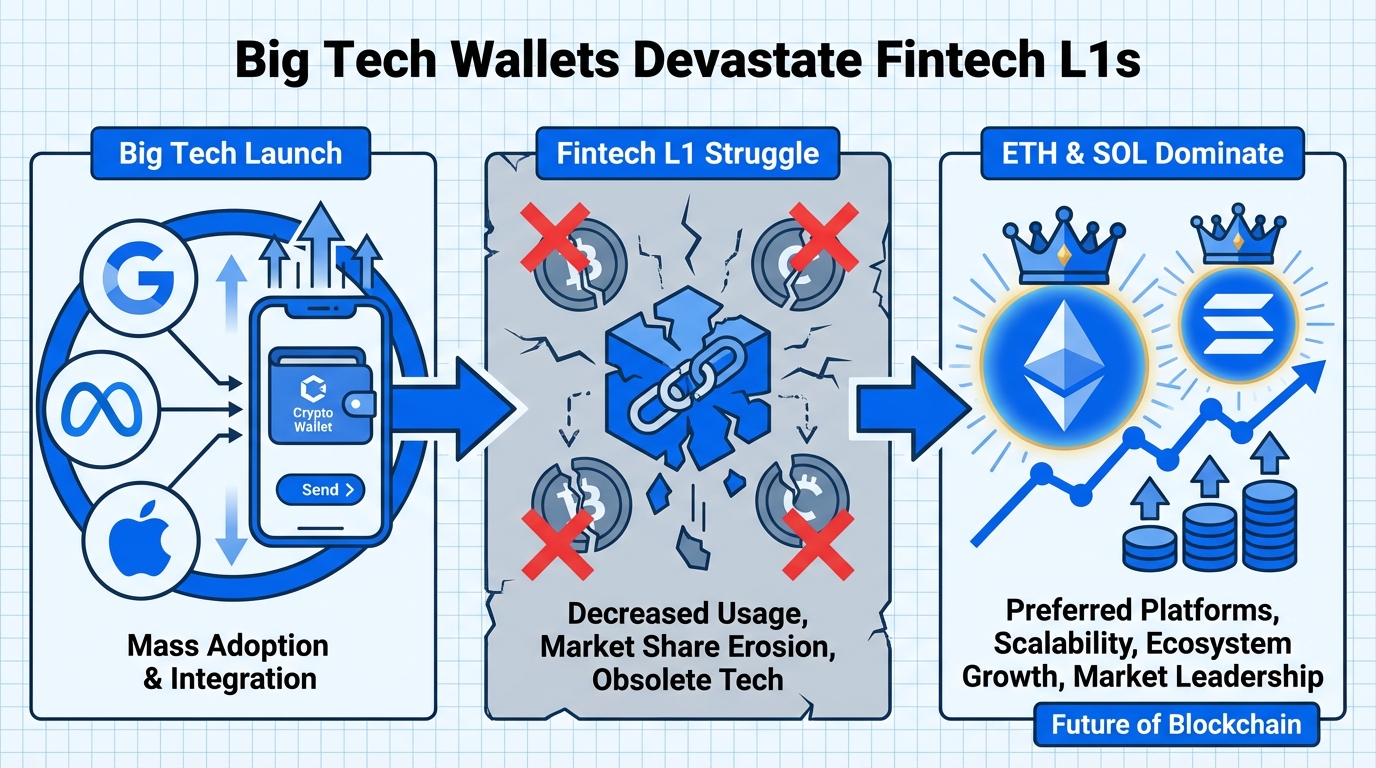

Big Tech Crypto Wallet Launch Could Devastate Fintech L1s as Ethereum and Solana Cement Market Leadership

Jon: Hey Lila, have you heard the latest buzz in the crypto space? According to recent predictions from Dragonfly’s Haseeb Qureshi, a major Big Tech company—like Google, Apple, or Meta—could integrate a native crypto wallet by 2026. This isn’t just some minor update; it’s poised to shake up the fintech world, especially those new Layer 1 blockchains trying to compete with giants like Ethereum and Solana.

Lila: Whoa, that sounds big. I’ve seen headlines about Big Tech eyeing crypto, but integrating wallets directly? That’s like your phone suddenly becoming a full-fledged bank. But Jon, why does this matter? Isn’t the crypto market already crowded?

Jon: Exactly, Lila. It matters because Big Tech has billions of users already locked into their ecosystems—think iOS or Android. If they add seamless crypto wallets, it could onboard masses without the friction of downloading separate apps. Recent reports suggest this could devastate fintech-launched Layer 1s, those custom blockchains from banking giants aiming to rival public ones. Ethereum still holds about 60% of DeFi market share, and Solana’s hitting revenue milestones like $1.5 billion. These public chains are cementing leadership, while fintech L1s might struggle to attract users. It’s not hype; it’s about distribution power.

Lila: Okay, that clicks. But let’s dig into the problem here. What’s the core issue with these fintech L1s that Big Tech could exploit?

Jon: The problem boils down to adoption and trust in a fragmented ecosystem. Fintech companies, like those in banking or payments, are launching their own Layer 1 blockchains—think of them as private highways built to handle financial traffic faster and cheaper than public roads like Ethereum or Solana. But here’s the rub: without massive user bases, these highways stay empty. Big Tech, with its billions of daily active users, could launch wallets that integrate directly with these public chains, bypassing the need for fintech’s custom ones. It’s like if Uber suddenly made its app the default for all city transport, leaving new taxi startups in the dust.

Lila: Empty highways—that analogy helps. So, fintech L1s are building infrastructure, but without the cars (users), it’s pointless. Can you clarify what makes public chains like Ethereum and Solana so sticky?

Jon: Sure. Imagine the crypto world as a busy city. Ethereum is like the old downtown with skyscrapers—it’s got robust smart contracts and a massive developer community, but traffic (high fees) can jam up during rush hour. Solana is the sleek new suburb with high-speed rail—faster transactions at lower costs, attracting apps in gaming and NFTs. Fintech L1s are trying to be exclusive gated communities, but they lack the network effects. Predictions from VCs like Dragonfly indicate that by 2026, more Fortune 100 firms will roll out blockchains, yet they’ll fail against public ones because users prefer open, battle-tested systems. It’s not about being first; it’s about being unavoidable.

Lila: Got it. So the “why” is really about ecosystem dominance. Big Tech’s entry could accelerate that by making crypto accessible to normies, right?

Under the Hood: How it Works

Jon: Alright, let’s peel back the layers. At its core, a crypto wallet is like a digital keyring—it holds private keys that let you sign transactions on a blockchain. Big Tech integrating this means embedding it into apps like Google Pay or Apple Wallet, potentially supporting chains like Ethereum (ETH) or Solana (SOL). Ethereum uses a proof-of-stake consensus, where validators stake ETH to secure the network, processing smart contracts—self-executing code for things like DeFi loans. Solana, on the other hand, employs proof-of-history, timestamping transactions for blazing speed, up to 65,000 TPS versus Ethereum’s 15-30 TPS.

Lila: Proof-of-what? Slow down—rephrase that for someone who’s not a blockchain ninja.

Jon: Fair point. Consensus is how the network agrees on truth without a central boss. Ethereum’s like a democracy where rich voters (stakers) decide; Solana’s like a clockwork factory where every part timestamps its work to keep everything in sync. Fintech L1s often mimic this but add proprietary tweaks for compliance, like built-in KYC. The devastation comes if Big Tech wallets default to public chains, starving fintech L1s of liquidity.

Lila: Okay, that makes sense. How do these compare side by side?

Jon: Let’s break it down in a table for clarity.

| Aspect | Fintech L1s | Ethereum | Solana |

|---|---|---|---|

| User Base Potential | Limited to fintech’s customers; struggles with adoption | Huge, with millions of wallets and dApps | Growing fast, especially in retail and memes |

| Transaction Speed/Cost | Customized for low fees, but untested at scale | Moderate speed; fees can spike to $10+ | Very fast; fees under $0.01 |

| Developer Ecosystem | Nascent; focused on enterprise | Vast, with Solidity as standard | Rust-based, attracting high-perf devs |

| Big Tech Impact | Could be sidelined as users stick to integrated wallets | Likely to benefit from easy onboarding | Positioned for mass adoption in apps |

Jon: See? The mechanics favor established players. Tokenomics play in too—ETH as gas for transactions, SOL for staking. Big Tech wallets could abstract this away, making it feel like Venmo but on-chain.

Lila: So who actually uses this? I mean, beyond traders, what’s the real-world application?

Jon: Great question. On the developer side, Ethereum powers DeFi protocols like Uniswap for decentralized trading or Aave for lending—think automated banks without bankers. Solana shines in high-throughput apps, like NFT marketplaces or real-time gaming, where speed matters. For users, Big Tech wallets could mean sending crypto as easily as texting, enabling cross-border payments or microtransactions in apps. Fortune 100 firms might use them for supply chain tracking, but the technical benefit is interoperability—your wallet works across ecosystems without silos. It’s about efficiency, not get-rich schemes.

Lila: Efficiency sounds practical. For fintech L1s, use cases might be internal, like faster settlements for banks?

Jon: Precisely. They could handle tokenized assets or CBDCs, but if Big Tech funnels users to public chains, those use cases stay niche. Worth watching how this evolves, as it could redefine fintech without overhyping.

Lila: Okay, if someone’s curious, how do they learn more without jumping in blindly? Like an action plan?

Jon: Let’s structure it. Level 1: Research and observation. Start by reading whitepapers—Ethereum’s at ethereum.org, Solana’s at solana.com/docs. Use explorers like Etherscan or Solscan to watch real transactions; it’s like peeking at a city’s traffic cams. Dashboards on Dune Analytics show metrics, helping you understand network health without any commitment.

Lila: That’s beginner-friendly. What about Level 2—actually trying it safely?

Jon: For hands-on, dive into testnets. Ethereum’s Sepolia or Goerli let you experiment with fake ETH—deploy a simple smart contract using Remix IDE. Solana has a devnet for testing Rust programs. It’s minimal-risk learning: set up a wallet like MetaMask or Phantom, play with dApps, and see mechanics in action. Remember, this is for education; real networks have volatility.

Lila: Perfect—no pressure, just exploration.

Jon: To wrap up, this Big Tech move could indeed challenge fintech L1s, solidifying Ethereum and Solana’s leads through sheer accessibility. But limitations persist—regulatory hurdles, scalability issues, and the ever-present crypto volatility.

Lila: Yeah, readers should remember: markets are unpredictable. Do your homework, understand the tech, and know risks remain high. It’s fascinating, but not a certainty.

Jon: Absolutely. Stay curious, stay informed.

About the Authors

Jon is a Web3 researcher with years of experience in blockchain architecture. Lila brings a fresh perspective, making complex topics accessible for all.

References

- Big Tech Crypto Wallet Launch Could Devastate Fintech L1s as Ethereum and Solana Cement Market Leadership

- Ethereum Official Site

- Solana Official Site

- Big Tech Crypto Wallets Coming by 2026, Fintech Blockchains Set to Struggle: Dragonfly

- Big Tech Will Integrate Crypto Wallets in 2026 — Dragonfly Exec